Changes to capital gains withholding

Current requirements

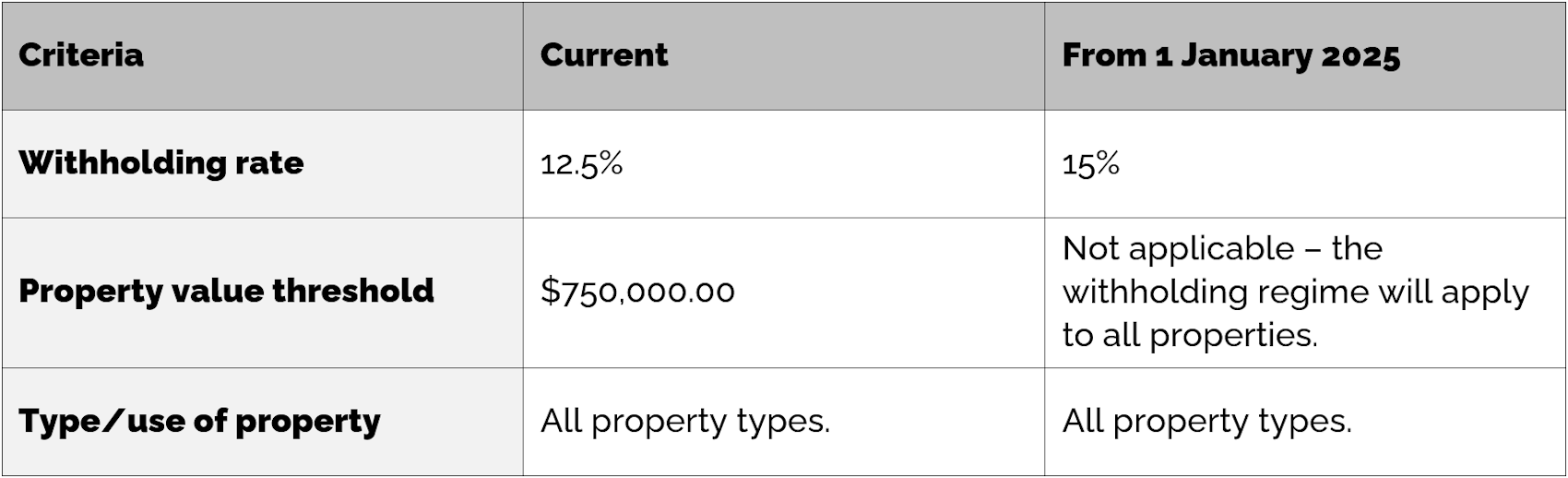

The foreign resident capital gains withholding regime (withholding regime) requires a person that is purchasing property to withhold 12.5% of the market value of the property and pay that amount directly to the ATO if:

- the relevant criteria apply to the sale; and

- the seller does not provide a Clearance Certificate to the person purchasing the property prior to settlement.

The withholding regime currently applies to all persons disposing of property with a market value of $750,000.00 or more.

Upcoming changes

With effect from 1 January 2025, the criteria will change so that the property value threshold of $750,000 is removed, meaning that all property sales will be subject to the withholding regime.

A summary of the current criteria and changes to take effect from 1 January 2025 are set out below:

What this means

All persons selling or disposing of a property will be required to provide a Clearance Certificate to the purchaser prior to settlement. If a Clearance Certificate is not provided, then the purchaser will be required to withhold 15% of the market value of the property from the sale price and pay that amount directly to the ATO on settlement.

If an amount is withheld, the seller will only receive any refund due after their next income tax return is processed by the ATO. The withheld amount may also be applied against any tax liability with the ATO.

The withholding regime continues to apply to all property types including, for example, a property that the seller occupies as their principal residence.

How we can help

If you are selling property in Tasmania, please get in touch with us and we will help you navigate the withholding regime, to ensure that funds are not withheld at settlement if you are not a foreign resident.