Climate-related financial disclosure requirements commence on 1 January 2025

On 17 September 2024, the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 (Cth) received Royal Assent, confirming the introduction of climate-related financial disclosure (CRFD) requirements in Australia from 1 January 2025.

What is the CRFD regime?

The CRFD regime will require reporting entities to submit a ‘sustainability report’ as part of their annual financial reports. The sustainability report will disclose how climate change could affect the company’s financial performance, operations and sustainability, and is designed to provide investors with the information they need to understand the financial impact of climate change on the companies in which they invest.

The sustainability report is required to include a climate statement (with accompanying notes) which complies with the Australian Sustainability Reporting Standards, to be made by the Australian Accounting Standards Board, and is expected to include the material climate-related financial risks and opportunities faced by the entity (if any), climate metrics and targets, including the entity’s Scope 1, 2 and 3 greenhouse gas emissions, and information relating to climate-related governance, strategy and risk-management.

In addition, a director’s declaration that the entity has taken reasonable steps to ensure the substantive provisions of its sustainability report are in accordance with the Corporations Act 2001 (Cth) is required to be provided.

When will the CRFD regime commence?

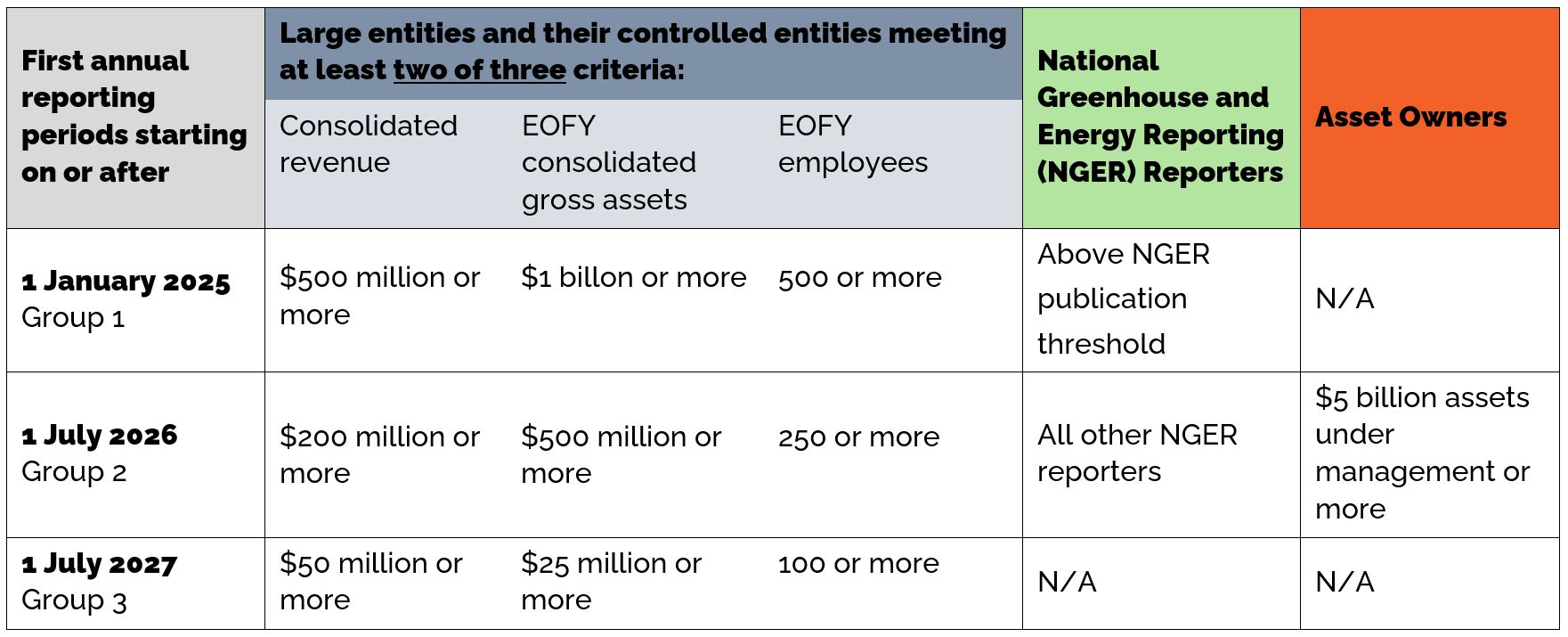

The CRFD regime will be progressively phased in over the next three years for the following groups of entities:

- large entities required to report under Chapter 2M of the Corporations Act 2001 (Cth);

- entities required to report under the National Greenhouse and Energy Reporting Act 2007 (Cth); and

- asset owners with over $5 billion in assets under management.

Use the table below to determine when your entity may be required to comply. The regime will apply to an entity for its first financial year commencing on or after the relevant date in the table.

What are your next steps?

If the CRFD regime will apply in future, we recommend that your entity starts putting into place the systems, processes and governance practices that will be required to meet the new climate reporting requirements.